Why big oil should get bigger

The case for consolidation and the danger of divestment

Over the weekend, this IEA chart has been making the rounds on social media, typically accompanied with commentary like this: evil oil and gas companies have been spending a tiny fraction of their income on renewables or other low carbon solutions. This is accompanied by an exhortation for these companies to do more, “stop lying”, or something to that effect.

Should oil and gas companies be in the renewables game? Bloomberg’s Matt Levine, in his newsletter Money Stuff, lays out three paths for fossil fuel businesses:

Do what you’ve always done. Drill lots of oil, acquire new leases, explore the deep ocean, make long-term investments in drilling technology, keep being an oil company, hope it all works out.

Pivot to renewables. Drill oil for now, but make your long-term investments in green energy; build wind farms or drill geothermal wells or whatever, so that in X years, when the world stops using oil, you will be able to sell whatever it does use.

Drill the oil you’ve got, but plan for decline. Stop making lots of new long-term investments in oil fields. Maximize current cash flow, and spend it on stock buybacks. Eventually, in X years, your cash flows will be zero, and you will close up shop gracefully. But in the meantime there is money coming in, and rather than waste it on drilling new oil fields, you give it back to shareholders.

I have seen many arguments for #2, but I always wonder why the fossil fuels industry is better suited at running renewable projects than actual renewables companies. While certain developments, like offshore wind, carry some engineering overlap with the skillsets of the majors, most of the time, fossil fuel companies have little to bring to the table.1

The key issue with the “Pivot to Renewables” option is this: we WANT big western oil companies to produce as much oil as possible — because they are so much better than the alternatives. To protect the environment, big oil should get bigger.

Who emits more, small producers or large producers?

A key component of “Pivoting to Renewables” is divestment: big oil should sell their oilfields and plow the cash into renewables. However, big oil companies pollute significantly less than smaller oil companies.

Large oil companies put tremendous emphasis on their safety and environmental culture, recognizing that both are vital to their long-term success and credibility. This has occurred due to growing public scrutiny, regulatory pressure, and an understanding of the business case for environmental responsibility.2

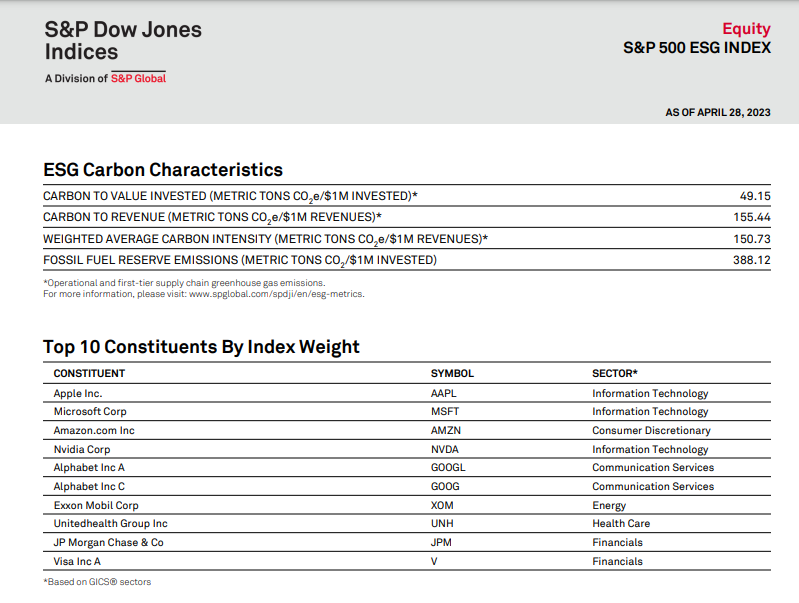

Let’s look at one specific mechanism nudging big, publicly traded oil companies to produce hydrocarbons with minimal pollution: ESG certifications.

The S&P 500 ESG Index tracks S&P 500 companies that meet carbon characteristics, like weighted average carbon intensity and fossil fuel reserve emissions. The number seven holding on that list? ExxonMobil. In fact, 5% of the index is in the energy sector:

Inclusion in these indexes provides a powerful pull on these oil and gas businesses, giving them access to institutional capital and supporting their share prices.

What impact does this have on the ground? Let’s focus on a key area where we have great data, the US Permian Basin. If the Permian were its own country, it would outrank Canada, Iran and Iraq, coming in at the #4 producer in the world. The EPA collects data on carbon emissions from oil and gas production, and the data clearly show that big producers emit less, and small producers emit more:

Big producers have the capital to build out gas infrastructure to reduce flaring and venting of associated gas (mostly methane produced alongside oil). They have the scale to generate meaningful returns across thousands of small valve repairs and facilities upgrades. And they have the investor community nudging them to invest in lower-intensity barrels in the first place. While I’ve just shown you the Permian above, the same trends holds across the US.

The problem of divestment and the power of sunlight

When a big oil company divests an oilfield, the production doesn’t simply disappear. Paradoxically, divestment can increase production. As the Harvard Business Review puts it:

Divestment by one party involves investment by another, which translates to more capital flowing to the fossil fuel sector, in contravention of the seller’s objectives.

When buying an oil and gas asset, the acquiring company comes in with plans to grow production, reduce costs, or both.

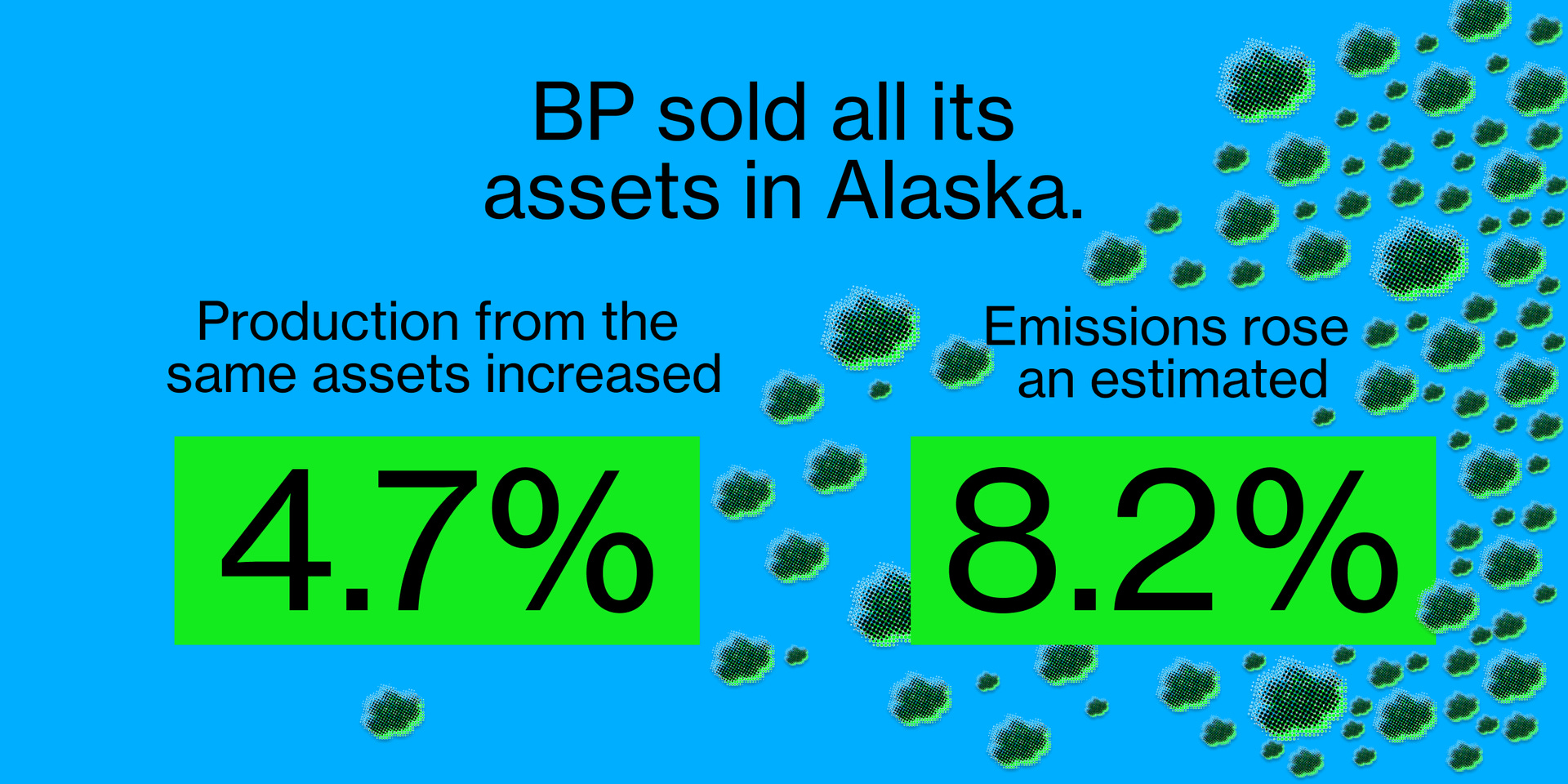

For a recent example, let’s look at BP’s divestment of its Alaskan business to private operator Hilcorp. Since the assets changed hands, production has risen nearly 5%, but emissions have risen even faster:

As Bloomberg puts it, “tracking carbon emissions becomes harder when big oil isn’t involved”.

This is not to speak ill of Hilcorp: they are doing the country and the world a service by continuing the operations of the North Slope’s strategic oil fields. Private companies play an in important role in the energy ecosystem, from drilling play-opening wildcats to pioneering new technologies and operating legacy fields. Hilcorp and other privates do, however, have a different set of incentives than BP, something that gets lost in monomaniacal pushes for divestment.

Scoreboard Politics

Recently, I have become obsessed with a concept that I’ll call “Scoreboard Politics.” The idea is simple—once you get it, you’ll see it everywhere.

As societies grow and become more complex, they gain all sorts of difficult-to-manage interest groups while slowly losing their governing capacity. Bureaucracies ossify, regulations accumulate, and powerful constituencies build ever-increasing stakes in the status quo. As real progress becomes more difficult, societies become less able to address the root causes of issues, so instead, they create the appearance of change by altering the scoreboard directly.3

In ancient times, this meant mandating the price of wheat, rather than improving farm productivity or establishing new trade routes. In modern times… well, I’m sure you can come up with a few examples.4

In demonizing big oil and encouraging its demise, society can score easy wins against industry leaders with few friends. But with every field that big oil divests, or every new development project that gets passed over by a major and picked up by a private operator, the environment faces a little more risk. Oil production moves into the shadows, operated without the healthy oversight of the public markets and pressure of institutional investors.

You can argue about oil demand growth and whether the industry, in aggregate, should increase or decrease production. But if protecting the environment is our goal, we should hope that big oil produces a larger share of hydrocarbons as time goes on.5 Rather than breaking up or shrinking big oil, we should encourage it to get bigger.

Let’s take a quick thought experiment. For a given $10 million in earnings, who would be better at allocating that cash to nuclear fusion research: the fossil fuel company who earned it or an investor? I say give it to the investor, who can invest it directly into fusion startups. Renewables are closer to core competencies of fossil companies than fusion, but they are still a far way from drilling oil or mining coal.

On a personal note, I have known many people from the biggest American oil companies: ExxonMobil, Chevron, and ConocoPhillips (where I started my career). The people working there are incredibly conscientious, earnest, and thoughtful. The cultures there are exactly what you would want in an oil and gas company.

I swear I read about this in a book at some point, but hours of (AI-assisted) internet searching turned up a blank. So if you can direct me to the actual originator of this concepts, I’ll be greatly appreciative. Olson’s The Rise and Decline of Nations has some of these concepts, but is mostly focused on the influence of price controls due to interest groups.

I try to avoid getting too political in the body of my essays, saving that stuff for the footnotes for only the die hards. Today, you can see “scoreboard politics” in our abandonment of school reform in favor of simply eliminating standardize testing requirements. I’d recommend you take a read through Matt Yglesisas’s important series on the death of school governance reform. To improve equitable outcomes across groups, the biggest thing we can do is give every child a great education. But that has just proven too difficult, so instead we are eliminating honors classes, watering down elite public schools, and removing SAT requirements for college admissions. Scoreboard politics!

Another prime example: pipelines. Denying a pipeline looks/feels great! But the oil will just get moved to market by rail or truck, which are less safe than a pipeline. Appearance of a victory, but on the ground, no improvement.

There is actually some hope that the market may take care of this itself. This chart from

shows that larger oil and gas companies are trading at a tremendous premium to smaller producers. If you’re Chevron, you can just buy the much smaller PDC—their production and earnings will be worth a lot more by receiving Chevron’s multiple.

Good stuff Ted. You covered a lot of ground here. I've had the same thought about oil and gas companies shifting to green energy-they aren't necessarily good at it and are using investors capital to experiment. I have excoriated Shell and BP for their feckless approaches to windfarms and solar, and even last mile energy distribution. They have no track record here and have burned billions upon billions of captial chasing this fantasy. Time will tell. I also agree with your comments about dumbing down for inclusivity and the bureaucratic state. Thanks for the thought-provoking article as always.